The trade finance process is the financing of exchange of commodities, finished goods and raw materials.

It makes import and export transactions possible for entities, ranging from a small business importing its first private-label product from overseas, to multi-national corporations.

Despite the explosive global trade growth, the trade finance industry hasn’t seen any significant change over the past decade.

In a typical trade transaction, the parties involved include banks, shippers, importers, exporters, regulatory bodies and the customs officers.

The parties are usually a part of the key verification point on the supply chain.

Also read about the Difference between Invoice Factoring and Invoice Discounting

Understanding Trade Finance

The main trade finance process function is to introduce a third-party to transactions to remove the payment risk and the supply risk.

It provides the exporter with receivables or payment according to the pre-agreement while the importer might be extended credit to fulfil the trade order.

Trade finance differs from conventional financing or credit issuance.

While applying for trade financing, you do not have to necessarily indicate a lack of funds as well as divulge liquidity issues as opposed to general financing which is used to manage solvency or liquidity.

Here are a few financial instruments used in trade finance:

- Banks can issue lending lines of credit to both importers and exporters.

- Letters of credit reduce the risk associated with global trade since the buyer’s bank guarantees payment to the seller for the goods shipped. However, the buyer is also protected since payment will not be made unless the terms in the LC are met by the seller. Both parties have to honour the agreement for the transaction to go through.

- Factoring is when companies are paid based on a percentage of their accounts receivables.

- Export credit or working capital can be supplied to exporters.

- Insurance can be used for shipping and the delivery of goods and can also protect the exporter from nonpayment by the buyer.

How do I secure trade finance?

Every lender has a criteria and specific requirements when advancing funds.

Most banks are very cautious on this as they look to have low risk, others less so, this, however, determines the interest and repayment rates.

1. Application

Truthful information is required when making the initial credit application as it drives the process.

This information also includes the type of information the business requires the cash for.

A good business plan is essential to show to a banker that your business idea is sound and realistic.

This plan will also show that you can implement it successfully and that you know exactly what the funds will be used for.

Business plans vary in formats, but usually include the following:

- A thorough introduction to the business, including a future vision and the goals of the business and any significant accomplishments to date.

- Information on the key stakeholders/ directors including past experience and equity make up of the company

- Introduction and an analysis of the product or service offered

- Overview of the sector/ competitor landscape

- Summary of anticipated results, including financial forecasts

Also, read about the Best Performing money market funds in Kenya

2. Negotiation

What you need to know is that before getting any trade finance loan, you need to negotiate terms that are suitable for you.

Get favourable terms and price that can be negotiated, this includes non-interest costs, fees and fixed charges as well as interest rates.

You need to first understand the structure of the fees and charges first as this will help you negotiate terms that are in your favour.

3. Evaluating the Application

A full credit risk assessment is usually run by the lender. This credit analysis will usually involve inputting figures from the applicant’s income statement, balance sheet and cash flow documents.

The analysis will also take into consideration the collateral the SME can provide and the quality of this.

The evaluation process will normally involve some kind of credit scoring process, taking into account any vulnerabilities such as the market the business is entering, probability of default and even the integrity and quality of management.

A credit score is normally ranked from AAA (very low risk of default) to D (likely to result in the denial of a loan application).

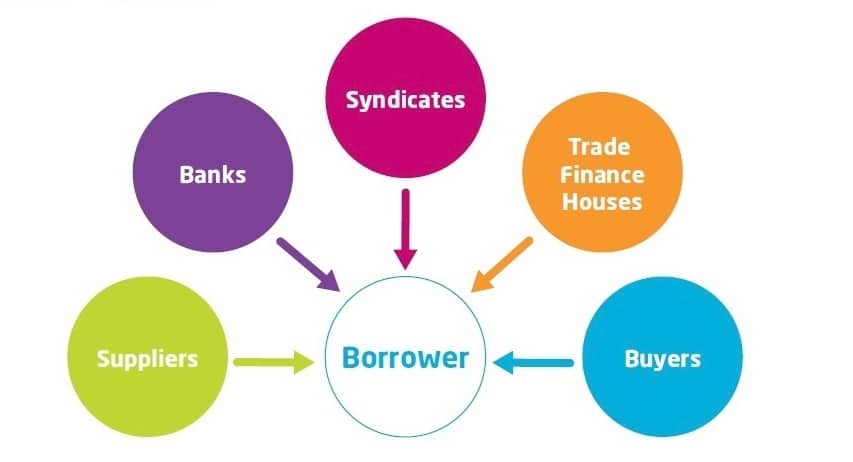

Providers of trade finance

As a form of risk mitigation, buyers and sellers can choose to use trade finance.

If a buyer or seller wants to finance a trade cycle funding gap, they need to look into trade finance.

A financier requires control of the use of funds, control of goods and source of repayments.

They also require visibility and monitoring over the trade cycle through the transaction.

Security over the goods and receivables is also required by the financier.

Also, read about What to do if a bank says no

CONCLUSION

In order to maintain a good relationship with the lender, repayment of an approved loan in a timely manner is essential (it also ensures the business has a good credit rating).

Reputation as a borrower is crucial when growing a business – finance facilities and trade funding may not be a one-time occurrence, and it can become easier and faster to get funding again once a company establish a good reputation and connection with their lender.

It is also important to remember the contractual and legal obligations that a company has, as per the loan agreement.